Global Instability & Fuel Price Impacts on Middle East Fleets

Major geopolitical events often leave a prolonged impact on the aviation industry . The escalating conflict in Iran has sent shockwaves, primarily by destabilizing global energy markets.

Fuel Prices & Airline Hedging

The price of oil per barrel has spiked from mid-$60 in early 2026 to over $100 per barrel by early March, and along with it, the price of jet fuel has risen. Based on IATA’s Jet Fuel Price Monitor, as of March 2026, jet fuel prices have surged beyond $150 per barrel, driven by fears and realities of supply disruptions in the Strait of Hormuz — a chokepoint for 20% of the world’s oil, according to the U.S. Energy Information Administration.

Airlines can offset the volatility of oil prices by using a common strategy — fuel hedging. By using financial derivatives such as future contracts or options, airlines can lock in fuel prices for future months or even years, allowing them better control over their near-term costs.

However, most U.S-based carriers discontinued their hedging programmes, with Southwest Airlines being the last to end the practice in March 2025. This will result in U.S. carriers being impacted sooner than others (1).

On the other hand, Asian and European carriers have temporary protections in place, with many hedging between 30% and 87% of their needs for at least H1 2026, and some even until the end of 2026. Some examples of hedged airlines include Air France-KLM, Air New Zealand, British Airways, Cathay Pacific, EasyJet, Iberia, Lufthansa, Qantas, Ryanair, TAP Portugal, and Wizz Air.

The rise in fuel prices has a flow-through impact not just on airlines but also on consumer goods and spending habits, which can impact passenger demand. Further, less fuel-efficient aircraft will be under greater scrutiny and higher risk for increased supply should airlines need to pull back on capacity.

Airspace Disruption

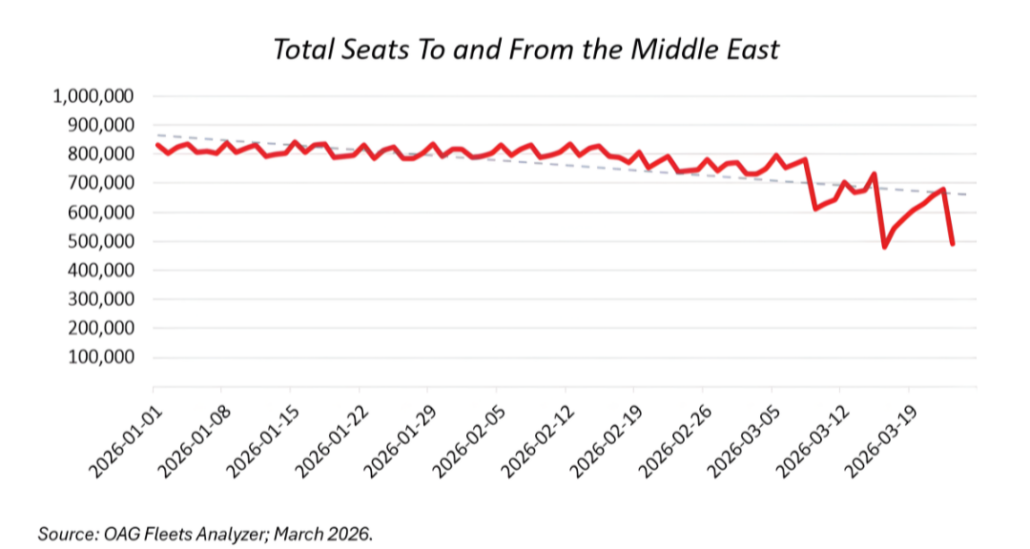

Looking at data from OAG Fleets Analyzer, prior to the Iran conflict, the total seat capacity entering and leaving the Middle East averaged 700,000-800,000 seats. However, as of March 2026, that has reduced to below 500,000 seats. This is evident as airlines cancelled numerous flights due to safety concerns, as well as the closure of various Flight Information Regions (FIR) in the Middle East.

(1) For further insight into the potential exposure, please refer to mba’s published article on U.S. carrier profitability from March 23, 2026.

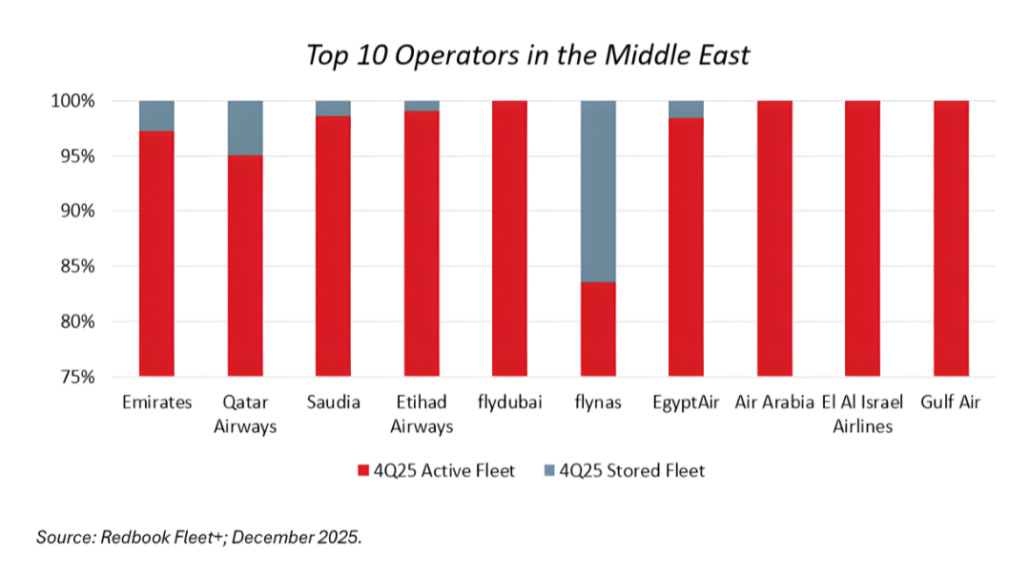

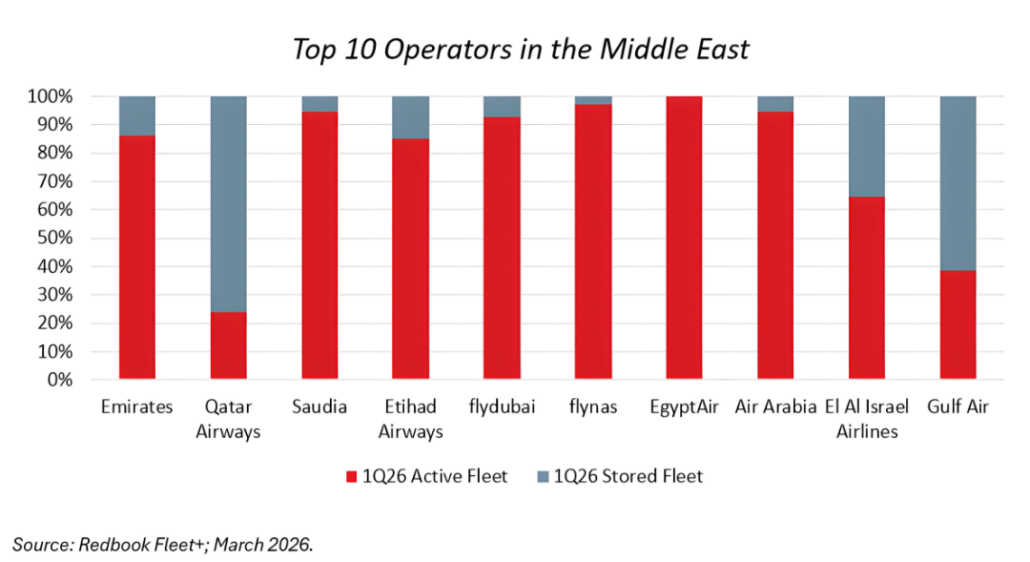

As the conflict continues to intensify with no clear resolution in sight, airlines, particularly in the Middle East, have taken precautionary measures and started storing their fleet. mba Aviation’s Fleet+ data shows that as of 4Q 2025, the average storage rate for the top 10 operators in the Middle East was around 3%. However, as of March 2026, that has gone up to 22%, a sevenfold increase.

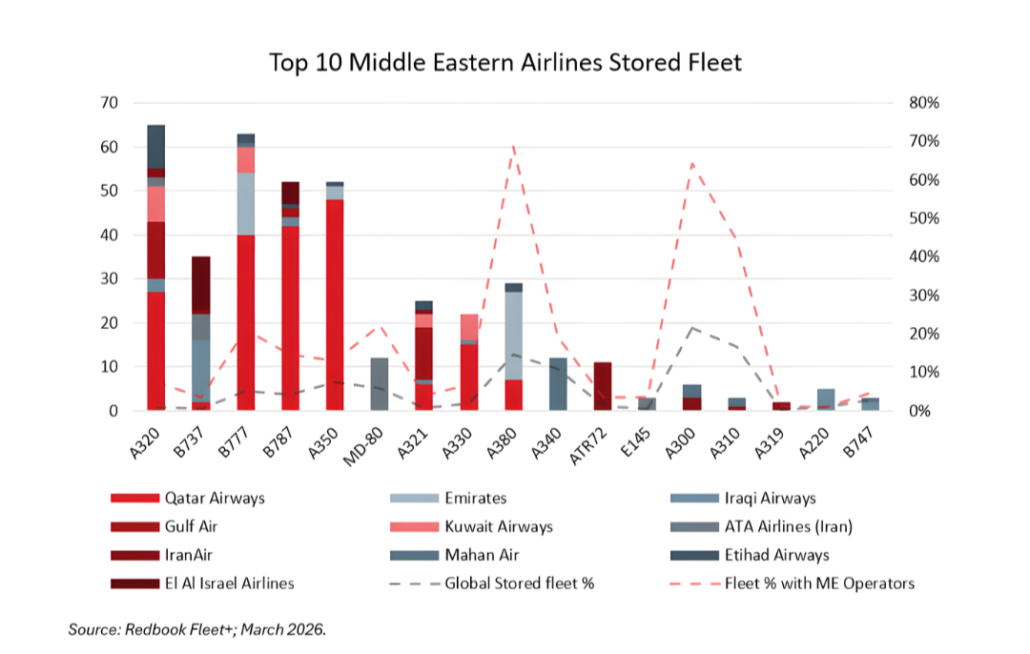

When we focus on just the stored fleet of the top 10 Middle East operators by fleet size, as of March 2026, the largest aircraft type to be in storage is the A320 (65 aircraft in storage), closely followed by 777 (63 in storage), 787 and A350 (52 aircraft each in storage), all of which are widebody aircraft. However, if we look at this in terms of the global fleet, only 1% of all A320s are in storage with Middle East operators, while the 777, 787, and A350 types account for 5%, 4%, and 7% respectively.

The impact of the current stage rates of the fleet in the Middle East is not that significant. However, there is a big inherent risk if the entire fleet of Middle East operators, particularly for the aircraft types mentioned above, all go into storage. Traditionally, the immediate impact usually falls on widebody aircraft, as they are operated on Long- or Ultra-long-haul routes. Data for mba Aviation’s Fleet+ shows the potential risk for the A380 is very high, with almost 70% of the fleet in the Middle East region, followed by the A300 (64% of the fleet in the Middle East) and the A310 (44% of the fleet in the Middle East).

Ultimately, the crisis in Iran serves as a stark reminder of how geopolitical stability is intertwined with global mobility. As airlines navigate these testing and turbulent times of rerouted paths and surging fuel costs, the industry’s resilience is once again being put to the test.

For further inquiries about anything covered in this article, please contact etamang@mba.aero.