https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-60.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2026-05-26 14:57:102026-05-26 14:57:10Left Hanging: The Critical Shortage of U.S. Airport Hangars

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-60.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2026-05-26 14:57:102026-05-26 14:57:10Left Hanging: The Critical Shortage of U.S. Airport Hangars https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-58.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2026-04-07 09:11:342026-04-07 15:57:23Global Instability & Fuel Price Impacts on Middle East Fleets

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-58.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2026-04-07 09:11:342026-04-07 15:57:23Global Instability & Fuel Price Impacts on Middle East Fleets https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-56.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

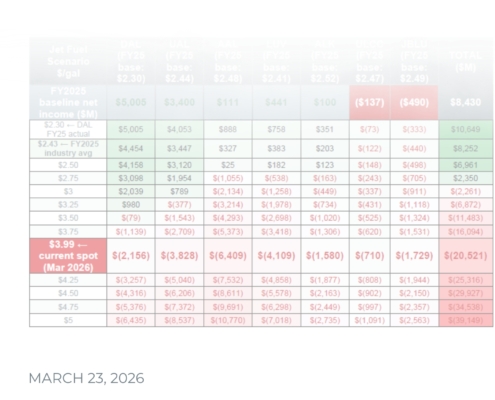

Jenn Atkins2026-03-23 14:25:122026-03-23 14:25:12Crude Awakening

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-56.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2026-03-23 14:25:122026-03-23 14:25:12Crude Awakening https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-25.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-11-14 16:03:062025-11-14 16:03:06MD-11 Grounding and the Air Cargo Capacity Crunch

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-25.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-11-14 16:03:062025-11-14 16:03:06MD-11 Grounding and the Air Cargo Capacity Crunch https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-23.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-09-17 14:07:232025-09-17 14:07:23The Value Add of Airline Loyalty Programs

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-23.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-09-17 14:07:232025-09-17 14:07:23The Value Add of Airline Loyalty Programs https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-48.png

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-08-11 17:30:362025-08-11 17:30:36A Look at LEAP-1A Engine High-Pressure Turbine Blades

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-48.png

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-08-11 17:30:362025-08-11 17:30:36A Look at LEAP-1A Engine High-Pressure Turbine Blades https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-13.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-05-30 14:01:472025-05-30 16:28:40Azul Seeks Restructuring Under Chapter 11: What It Means for Lessors and Lease Rates

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-13.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-05-30 14:01:472025-05-30 16:28:40Azul Seeks Restructuring Under Chapter 11: What It Means for Lessors and Lease Rates https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-6.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-05-15 15:29:082025-05-15 15:29:08The Market Message in 1Q2025 U.S. Airlines Earnings

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-6.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-05-15 15:29:082025-05-15 15:29:08The Market Message in 1Q2025 U.S. Airlines Earnings https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-5.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-05-09 11:55:262025-05-12 15:03:02Tariffs are the Headline, Uncertainty is the Story: How Appraisers are Looking at the Tariffs

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-5.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-05-09 11:55:262025-05-12 15:03:02Tariffs are the Headline, Uncertainty is the Story: How Appraisers are Looking at the Tariffs https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-04-29 16:20:282025-05-07 15:00:40Margins in Turbulence: The Overlooked Role of Crack Spreads in Airline Earnings

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf.jpg

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-04-29 16:20:282025-05-07 15:00:40Margins in Turbulence: The Overlooked Role of Crack Spreads in Airline Earnings