https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-38.png

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-04-23 12:06:522025-05-05 14:44:38Too Many Planes, Not Enough Runways

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-38.png

2000

1545

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-04-23 12:06:522025-05-05 14:44:38Too Many Planes, Not Enough Runways https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-26.png

6250

4830

Avery Smith

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Avery Smith2025-02-10 14:26:002025-03-21 16:33:50U.S. Airline Cost Migration

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-26.png

6250

4830

Avery Smith

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Avery Smith2025-02-10 14:26:002025-03-21 16:33:50U.S. Airline Cost Migration https://www.mba.aero/wp-content/uploads/Screenshot-2025-01-23-091818.png

483

933

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-01-23 09:54:412025-07-02 15:16:48Global High-Risk Categories: A Look at Midair Collisions and Near Misses

https://www.mba.aero/wp-content/uploads/Screenshot-2025-01-23-091818.png

483

933

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-01-23 09:54:412025-07-02 15:16:48Global High-Risk Categories: A Look at Midair Collisions and Near Misses https://www.mba.aero/wp-content/uploads/Leased-vs-Owned-2025-01-23-094212.png

560

1002

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

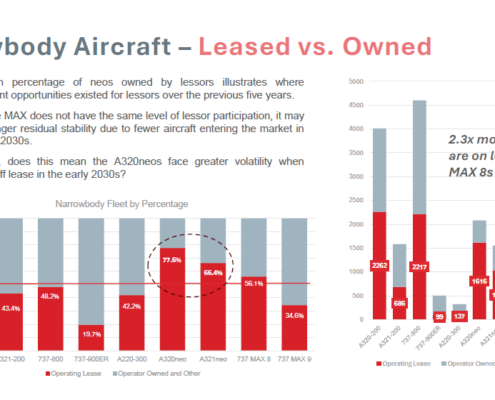

Jenn Atkins2025-01-23 09:52:182025-01-23 09:52:18Narrowbody Aircraft – Leased vs. Owned

https://www.mba.aero/wp-content/uploads/Leased-vs-Owned-2025-01-23-094212.png

560

1002

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-01-23 09:52:182025-01-23 09:52:18Narrowbody Aircraft – Leased vs. Owned https://www.mba.aero/wp-content/uploads/CommercialAircraftFleetForecastSS.png

811

622

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-01-22 13:41:422025-02-11 17:13:45Commercial Aircraft Fleet Forecast

https://www.mba.aero/wp-content/uploads/CommercialAircraftFleetForecastSS.png

811

622

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2025-01-22 13:41:422025-02-11 17:13:45Commercial Aircraft Fleet Forecast https://www.mba.aero/wp-content/uploads/Screenshot-2024-10-17-145532.png

713

550

Megan Gibson

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Megan Gibson2024-10-17 14:51:002025-02-11 17:08:47The Boeing Machinist Strike

https://www.mba.aero/wp-content/uploads/Screenshot-2024-10-17-145532.png

713

550

Megan Gibson

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Megan Gibson2024-10-17 14:51:002025-02-11 17:08:47The Boeing Machinist Strike https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-25.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2024-06-12 15:18:472025-03-21 16:31:03How Much Does Ownership Really Cost an Investor?

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-25.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2024-06-12 15:18:472025-03-21 16:31:03How Much Does Ownership Really Cost an Investor? https://www.mba.aero/wp-content/uploads/Screenshot-2024-06-12-105231.png

690

1263

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2024-06-12 10:54:592025-03-24 09:29:16mba Aircraft Ranking Score Changes Cont.

https://www.mba.aero/wp-content/uploads/Screenshot-2024-06-12-105231.png

690

1263

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2024-06-12 10:54:592025-03-24 09:29:16mba Aircraft Ranking Score Changes Cont. https://www.mba.aero/wp-content/uploads/Screenshot-2024-06-12-104757.png

707

1264

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

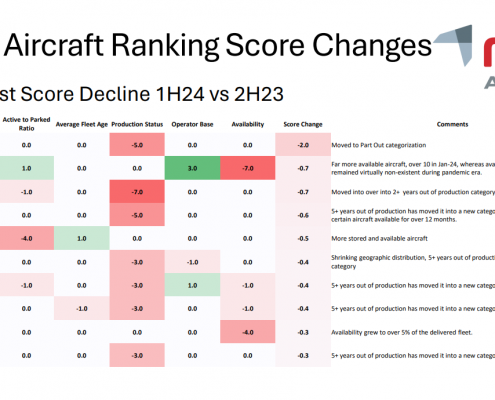

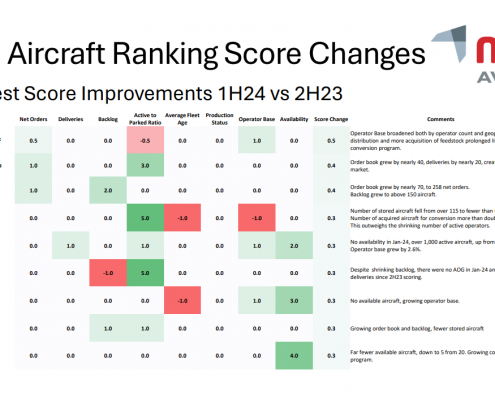

Jenn Atkins2024-06-12 10:51:462025-03-24 09:30:19mba Aircraft Ranking Score Changes

https://www.mba.aero/wp-content/uploads/Screenshot-2024-06-12-104757.png

707

1264

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2024-06-12 10:51:462025-03-24 09:30:19mba Aircraft Ranking Score Changes https://www.mba.aero/wp-content/uploads/Engine-May-2024-Insight.png

901

697

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2024-05-28 15:59:442025-03-12 15:59:43Narrowbody Engine Values as a Proportion of Aircraft Values

https://www.mba.aero/wp-content/uploads/Engine-May-2024-Insight.png

901

697

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2024-05-28 15:59:442025-03-12 15:59:43Narrowbody Engine Values as a Proportion of Aircraft Values