https://www.mba.aero/wp-content/uploads/MarketAnalysisSnip.png

804

621

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2024-03-08 13:17:372025-03-12 17:29:27Supply & Demand – Market Analysis (March 2024)

https://www.mba.aero/wp-content/uploads/MarketAnalysisSnip.png

804

621

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2024-03-08 13:17:372025-03-12 17:29:27Supply & Demand – Market Analysis (March 2024) https://www.mba.aero/wp-content/uploads/WarsawAirportinsight.png

808

622

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-12-13 11:32:332025-03-13 17:26:26The New Warsaw Airport: “To Be or Not to Be?”

https://www.mba.aero/wp-content/uploads/WarsawAirportinsight.png

808

622

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-12-13 11:32:332025-03-13 17:26:26The New Warsaw Airport: “To Be or Not to Be?” https://www.mba.aero/wp-content/uploads/Untitled-design-75.png

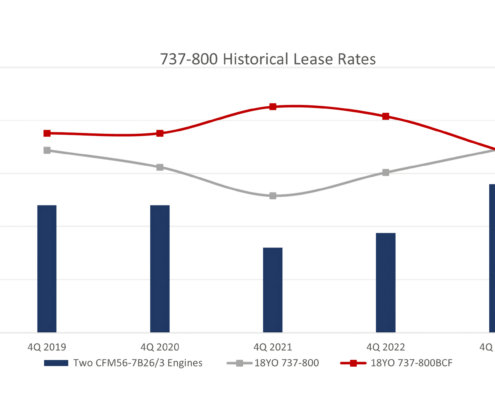

2035

3375

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-10-24 16:27:202025-03-18 14:28:07737-800 Passenger and Converted Freighter Lease Rates

https://www.mba.aero/wp-content/uploads/Untitled-design-75.png

2035

3375

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-10-24 16:27:202025-03-18 14:28:07737-800 Passenger and Converted Freighter Lease Rates https://www.mba.aero/wp-content/uploads/ScreenshotInsight1023.png

791

613

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-10-09 17:17:552025-03-17 15:06:56GTF HPT Inspection Operational Impact

https://www.mba.aero/wp-content/uploads/ScreenshotInsight1023.png

791

613

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-10-09 17:17:552025-03-17 15:06:56GTF HPT Inspection Operational Impact https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-27.png

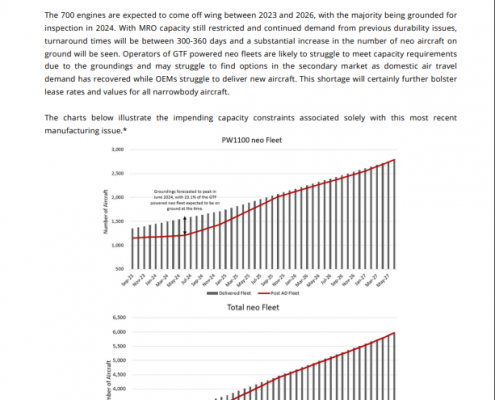

6250

4830

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-08-09 14:01:062025-03-21 16:36:56737-800 Market Profile – August 2023

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-27.png

6250

4830

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-08-09 14:01:062025-03-21 16:36:56737-800 Market Profile – August 2023 https://www.mba.aero/wp-content/uploads/Thumbnail-Website.png

746

577

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-07-21 17:30:312023-07-21 17:31:13Air Service Development: City Pair Trends

https://www.mba.aero/wp-content/uploads/Thumbnail-Website.png

746

577

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-07-21 17:30:312023-07-21 17:31:13Air Service Development: City Pair Trends https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-28.png

6250

4830

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-07-11 17:14:522025-03-21 16:39:39A320-200 Market Profile – July 2023

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-28.png

6250

4830

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-07-11 17:14:522025-03-21 16:39:39A320-200 Market Profile – July 2023 https://www.mba.aero/wp-content/uploads/ParisInsightImage.png

740

572

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-06-15 17:35:112023-06-28 15:17:14Market Analysis: Inflation Offering Orderbook Solutions?

https://www.mba.aero/wp-content/uploads/ParisInsightImage.png

740

572

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-06-15 17:35:112023-06-28 15:17:14Market Analysis: Inflation Offering Orderbook Solutions? https://www.mba.aero/wp-content/uploads/Part135Mandate.jpg

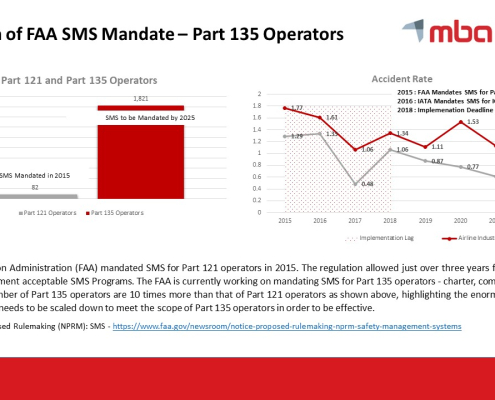

720

1280

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-02-06 10:06:192025-03-18 14:32:53Expansion of FAA SMS Mandate – Part 135 Operators

https://www.mba.aero/wp-content/uploads/Part135Mandate.jpg

720

1280

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2023-02-06 10:06:192025-03-18 14:32:53Expansion of FAA SMS Mandate – Part 135 Operators https://www.mba.aero/wp-content/uploads/DronesInEnergy_Pic.png

811

626

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2022-10-24 12:01:302022-10-24 12:01:30Drones in Energy: Safety Considerations for UAS in Industrial Inspections

https://www.mba.aero/wp-content/uploads/DronesInEnergy_Pic.png

811

626

kkmbaaero

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

kkmbaaero2022-10-24 12:01:302022-10-24 12:01:30Drones in Energy: Safety Considerations for UAS in Industrial Inspections