April 29, 2025

Margins in Turbulence: The Overlooked Role of Crack Spreads in Airline Earnings

mba Airline & Airport Services

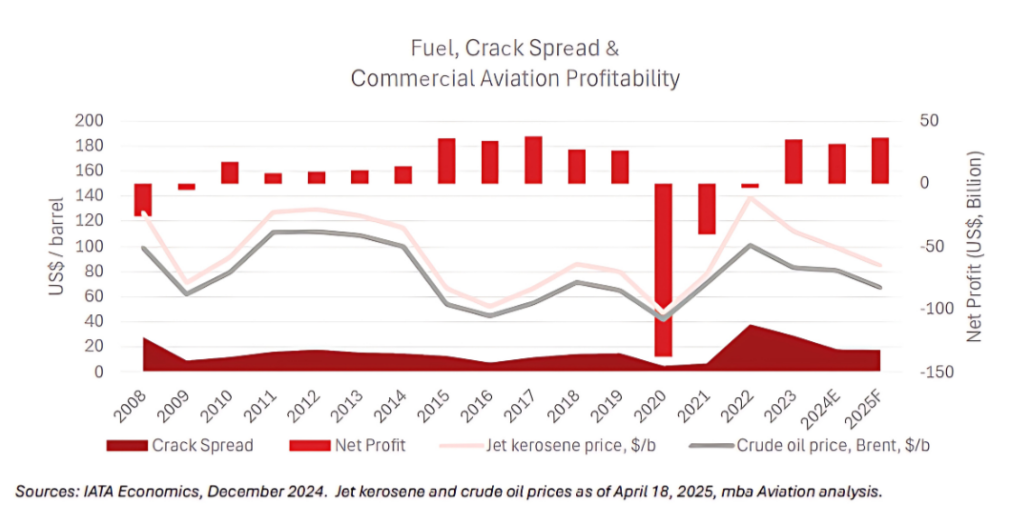

Fuel Price Recovery After COVID-19 Drove a Profitability Whiplash

Historically, lower jet fuel prices have correlated with higher airline industry profitability and vice versa. However, this relationship decoupled in 2020, when commercial aviation profitability plummeted to record lows, despite jet fuel prices falling to multi-year lows. This break in correlation was driven by COVID-19’s devastating impact on both global pol demand and air travel. In 2021 and 2022, industry losses narrowed even as fuel prices surged, with jet kerosene peaking at ~$170/b in 2022. Profitability in those years was supported more by yield strength and cost discipline than by fuel cost relief.

Jet Fuel Often Rises Faster Than Crude Oil (Especially Post-2021)

The jet fuel crack spread widened significantly in 2022-2023, indicating refining bottlenecks and supply chain pressure. Jet fuel prices outpaced crude oil, rising to nearly ~40.0% above Brent in 2022. This divergence highlights how jet fuel pricing has become increasingly volatile and decoupled from crude, due largely to constrained refining capacity. This introduces added complexity for airlines managing fuel hedging strategies.

Fuel Costs Do Not Fully Explain Profitability Trends

During 2015-2019, with fuel prices at moderate levels, airline profitability peaked, supported by strong demand, low costs, and low-cost carrier expansion. Yet from 2022 to 2025, even amid high fuel costs and elevated crack spreads, airline net profit has remained positive. This suggests the industry has become more resilient, enabled by consolidation, COVID-19-era restructuring, and newer, more efficient fleets, though this resilience has its limits.

Forecasts Suggest Pressure on Margins

While both jet fuel and crude oil prices are expected to moderate in 2024-2025, net profit is forecast to remain flat. This points to softening demand and limited pricing flexibility, even with fuel relief. The industry may be entering a period of margin compression, where easing costs are offset by plateauing revenue growth.

Long-Term Structural Challenge: Crack Spreads Aren’t Going Away

Crack spreads have remained elevated since 2022, despite falling oil prices. This may reflect structural refining constraints, particularly for aviation-grade fuels. For airlines, this signals a new normal of higher refining margins, requiring more sophisticated fuel management and strategic planning.