February 9, 2021

Narrowbody Engine Q1 2021 Update: CFM and IAE Shop Visit Forecast and Values

by Garrick Rice

During the pandemic the narrowbody engine MRO space has seen a drastic reduction in numbers of serviced engines. The primary cause is the loss in domestic capacity as airlines look to defer maintenance to offset their revenue loss by reducing all possible variable and fixed costs. Up to this point, airlines that have the capacity to do so have been successful in consuming under-utilized engines or flying domestic aircraft at lower monthly utilization to avoid expensive long-term storage and maintenance costs. This necessary adaptation of fleet utilization has disrupted the well-defined trajectory of engine shop inductions, reducing engine MRO’s capacity, and ultimately effecting market values for narrowbody engines.

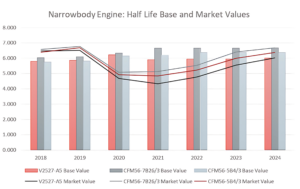

In the years leading up to the COVID-19 pandemic, market values for the CFM56-5B/&B and V2500-A5’s (IAE) engines were trading above base value. Boeing and Airbus’s ability to produce new technology aircraft couldn’t match the increasing levels of airline traffic. A further driver of demand was the delays in delivery of next generation aircraft, 737 MAX groundings and in-service issues of new technology engines. There was also increasing levels of maintenance required in 2020-2024. These two factors kept all aspects of the engine’s value drivers high, which included lease and maintenance reserve revenue, Core + QEC value, and LLP values during this period as buying increased in anticipation of the program’s strongest years of the demand. Engine lessors looked to capitalize on bridging any downtime to conduct this maintenance, while MRO’s and material distributors looked to increase parts inventory to offer reduced material costs to airlines and lessors.

The loss in domestic passenger demand has caused a vast under-utilization of narrowbody engines at the fleet level. This lower monthly utilization alone has adjusted the scheduled maintenance events that can be expected until mass immunization and passenger confidence return. The rate at which this confidence will return is the ultimate driving force of MRO expectations and engine values as a whole.

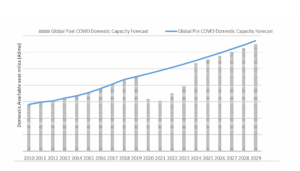

Global air traffic capacity is down ~70% for 2020 compared to the figures achieved in 2019. While the domestic markets were less effected than international travel, there is more volatility than certainty as we enter the third phase of the pandemic. This uncertainty has translated into large bid-ask spreads for assets currently available and limited market participants. mba’s estimations are that all global domestic travel ~38% lower in 2021 than expected pre-pandemic with continued underperformance until 2024.

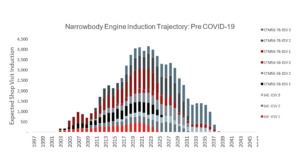

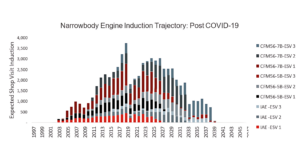

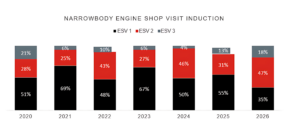

MRO expectations have adjusted alongside the expectation of domestic travel in the coming years. Fleet wide under-utilization, expected aircraft retirements, and airline maintenance avoidance has caused an expected ~49% drop in engine inductions expected in 2021. Given the low demand forecast, early retired aircraft are likely to be disassembled, and the engines utilized as green time spares before moving to part out. This will likely have lasting effects on the total levels of shop visit inductions that will resemble 2017 figures. These total annual engine induction figures could be sustained from 2023-2027 before decline thereafter.

In efforts to match demand some MRO’s have offered early retirements, downsized, or off-loaded operational locations, and in some instances have cut labor force. The highly skilled nature of aircraft and engine mechanics saw labor shortages during the years leading up to the pandemic. This labor gap and retraining efforts could potentially increase turnaround times even in a low MRO demand environment.

While the absolute age of 737NG and A320CEO programs are nearing retirement, the vast majority of these aircraft were delivered from 2008-2017. During this period the introduction of major design upgrades such as the Tech Insertion for the CFM engines and the SelectOne modifications in the IAE engines became build standards. Operational efficiency increased as the new technology in the hot sections reduced temperature and ultimately extended the on-wing interval achieved. Even as the shop visit forecasted has been distributed by the COVID-19 pandemic, the majority of engine events to take place until 2025 are the first shop visit.

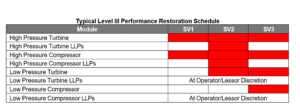

Shop visit schedules assume Level III performance restorations in the High Pressure Turbine (HPT) and High Pressure Compressor (HPC) modules during the first induction (SV1), Level III performance restorations in the HPT, HPC, and Low Pressure Turbine (LPT) modules the second induction (SV2), and Level III performance restorations in the HPT, HPC, and Low Pressure Compressor (LPC) modules during the third induction (SV3). High Pressure Turbine and High Pressure Combustion LLP’s replacements are assumed on the second scheduled maintenance (Low Pressure Turbine LLP parts are replaced at operator or lessor discretion).

The third and likely final shop visit assumes Lower Pressure Combustion and Low Pressure Turbine LLPs are replaced depending on cost allocation and continued use assumption. mba’s aircraft retirement analysis causing distribution to the expected induction schedules assumes that older aircraft are retired first and that these aircraft will have +/- 30% of their engines between SV2-SV3 on average with the remainder +/- 70% of their engines being beyond SV3.

Given the expected increase and maintenance status of available engines, coupled with the fact that the majority of forecasted inductions will be SV1 where material and the majority of the will be focused in the HPC/HPT modules, there has been a split in market pricing pressure for serviceable and unserviceable engines. Unserviceable engines that would traditionally be acquired to reduce material cost for incoming engine inductions could spend lengthy time as inventory, as established buyers have increased inventory positions in the years building up to the pandemic and likely have ample supply given the current environment. The LLP value in these unserviceable engines has the potential to soften in short term as most of the engine events are SV1 and these are typically non-LLP replacement events. The long-term value of these components will remain stable as demand and escalation will outpace supply similar to the pre-pandemic market dynamics.

Green time engines are seeing less of a decline in market value as anticipation of the demand for leased assets during the recovery remains high. Possible MRO bottlenecks in the event of better-than-expected passenger demand has further potential to increase the value of these assets in the short term.

While narrowbody engines are currently trading near distressed price levels, the expectation of value recovery will likely supersede that of whole aircraft. Airlines looking to capture any uptick in capacity demand will require leased assets to fill the gap between expenditure deferrals and lack of MRO slot availability.

While the unserviceable engine market may be challenged for the foreseeable future, the expectation of the leasing market could rapidly stabilize market values from their current levels. Given the position of the fleet within its maintenance cycle, base value readjustments due to the COVID-19 pandemic will be solely correlated to the return of domestic travel and are unlikely at this time.

2018-2021 Actual Values : 2022-2024 Projected Values