July 15, 2020

US Airlines’ Effort to Manage Liquidity

by Steven Harokopus

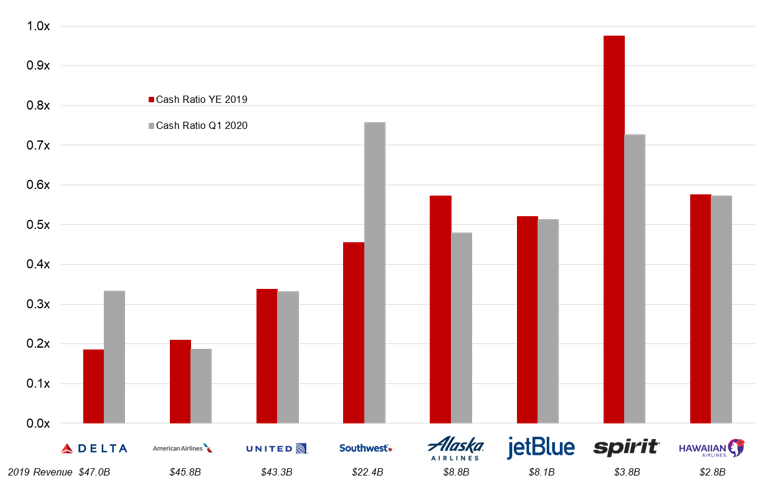

The COVID-19 Pandemic has pushed air travel demand to historic lows for the first half of 2020 and led to widespread groundings that have shocked the industry’s passenger revenues. Many US airlines have seen ticket refunds outpace net revenue and prompted management to raise capital and implement changes to reduce cash burn. US carriers drew down credit lines and secured billions in new financing during the first quarter of 2020 as the initial downturn of the pandemic hit. Airlines moved quickly to bolster their balance sheets with cash. The table below shows the cash ratio for the eight largest US passenger airlines. The cash ratio is a measure of liquidity that compares the firm’s available cash to its near-term liabilities. Although it is not always a widely used credit metric this ratio presents an interesting look at how management teams are handling this crisis as cash flow from operations has widely stopped. First quarter results indicate that for many of the subject airlines the cash ratio has slipped. Alternatively, Southwest Airlines went into the crisis with a strong balance sheet and was able to quickly secure additional long-term financing that bolstered the firm’s cash ratio.

As second quarter results are reported, we expect to see the cash ratios improve as management teams have made significant progress securing long-term financing, managing costs through schedule changes and voluntary employee leave, and generating cash receipts as we begin to see a slight uptick in demand from the VFR and leisure segments. During the second quarter, all of the airlines above have been successful in raising capital by encumbering assets to shore up balance sheets and refinance short-term debt. Delta, American, and JetBlue have collectively raised over $6.7 billion secured by its Frequent Flyer Program, Mileage Plus Holdings, LLC (“PH”). Another significant factor improving airline liquidity is US government aide through the CARES PSP program. US airlines agreed to delay involuntary furloughs, continue service on the underserved domestic routes, and limit financial engineering and executive compensation in return for grants and low interest loans from the US Treasury. The Treasury Department anticipates over $22B in total payroll support for the Subject airlines. Payroll support will keep routes open and airline staff employed as the carriers work to make travelers feel safe again.

All of the subject airlines have reported improvements in cash burn rates as the pandemic continues. Delta and American have reported improvements in cash burn rates as the pandemic continues. Delta and American have even set the ambitious target of approximately zero cash burn by the end of 2020. The Covid-19 crisis has seen many employees across the industry taking voluntary leave or accepting early retirement packages. Management teams have made significant progress in deferring or eliminating capital expenditures and non-essential projects. Raising long-term funds and taking creative approaches to preserving cash is going to be essential for the US carriers to continue operation and capture demand as it recovers.