https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-12.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2021-02-09 14:58:452025-03-18 15:48:55Narrowbody Engine Q1 2021 Update: CFM and IAE Shop Visit Forecast and Values

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-12.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2021-02-09 14:58:452025-03-18 15:48:55Narrowbody Engine Q1 2021 Update: CFM and IAE Shop Visit Forecast and Values https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-14.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-09-11 17:47:522025-03-18 16:47:05Corporate Jet Market Conditions – 1H20

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-14.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-09-11 17:47:522025-03-18 16:47:05Corporate Jet Market Conditions – 1H20 https://www.mba.aero/wp-content/uploads/Untitled-design-87.png

1967

3375

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

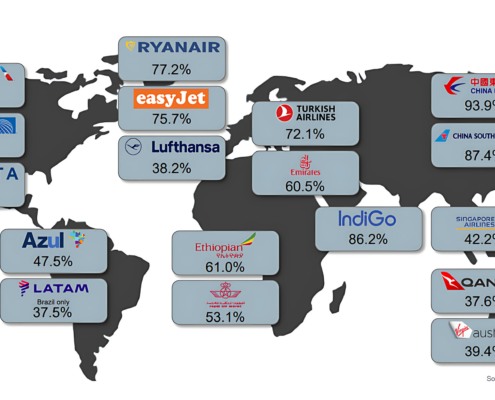

Jenn Atkins2020-08-26 16:59:092025-03-24 09:43:47How Many Aircraft did Major Airlines Operate Last Week?

https://www.mba.aero/wp-content/uploads/Untitled-design-87.png

1967

3375

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-08-26 16:59:092025-03-24 09:43:47How Many Aircraft did Major Airlines Operate Last Week? https://www.mba.aero/wp-content/uploads/Untitled-design-88.png

1626

3375

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-08-18 12:57:012025-03-18 16:56:31U.S. Air Operator Safety Trend

https://www.mba.aero/wp-content/uploads/Untitled-design-88.png

1626

3375

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-08-18 12:57:012025-03-18 16:56:31U.S. Air Operator Safety Trend https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-19.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-08-17 14:12:272025-03-21 11:42:00Evaluating the Airbus A220 and its Competition

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-19.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-08-17 14:12:272025-03-21 11:42:00Evaluating the Airbus A220 and its Competition https://www.mba.aero/wp-content/uploads/RASM-and-Capacity-Chart-e1597431675860.png

277

500

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

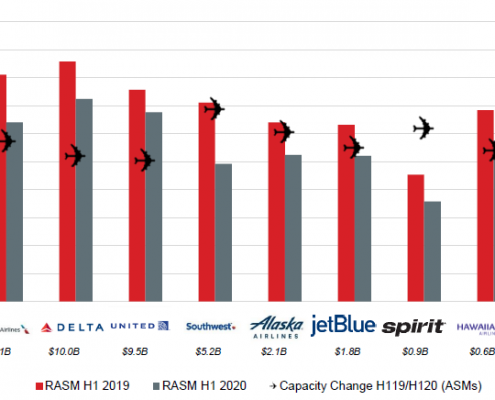

Jenn Atkins2020-08-14 15:26:002025-03-24 10:00:00Impact of Covid-19 on Capacity Planning and Revenues

https://www.mba.aero/wp-content/uploads/RASM-and-Capacity-Chart-e1597431675860.png

277

500

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-08-14 15:26:002025-03-24 10:00:00Impact of Covid-19 on Capacity Planning and Revenues https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-20.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-07-31 16:24:452025-03-21 13:42:10Evaluating the Boeing 787’s Backlog and Competition

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-20.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-07-31 16:24:452025-03-21 13:42:10Evaluating the Boeing 787’s Backlog and Competition https://www.mba.aero/wp-content/uploads/200720-LinkedIn-teaser-for-delivery-rate-drop-insight-e1595289898604.jpg

340

500

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

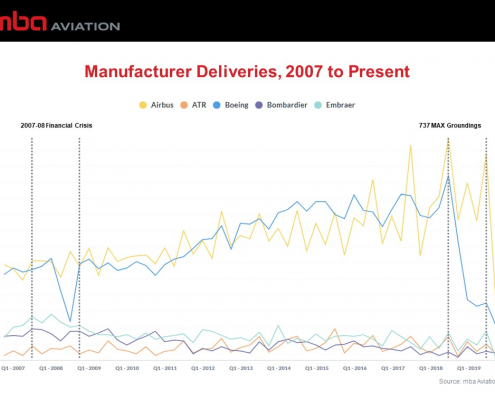

Jenn Atkins2020-07-20 14:50:142025-03-24 10:24:25Trends in OEM Delivery Rates

https://www.mba.aero/wp-content/uploads/200720-LinkedIn-teaser-for-delivery-rate-drop-insight-e1595289898604.jpg

340

500

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-07-20 14:50:142025-03-24 10:24:25Trends in OEM Delivery Rates https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-23.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-07-15 10:42:252025-03-21 16:14:44US Airlines’ Effort to Manage Liquidity

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-23.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-07-15 10:42:252025-03-21 16:14:44US Airlines’ Effort to Manage Liquidity https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-24.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-05-13 14:52:012025-03-21 16:25:10Utilization Reductions due to Groundings Impact Maintenance Cash Flows

https://www.mba.aero/wp-content/uploads/Front-Page-Insights-TEMPLATE.pdf-24.png

6250

4830

Jenn Atkins

https://www.mba.aero/wp-content/themes/enfold-child/images/Header-Logo-Solid.svg

Jenn Atkins2020-05-13 14:52:012025-03-21 16:25:10Utilization Reductions due to Groundings Impact Maintenance Cash Flows